The real estate market fallout from the response to the COVID-19 crisis has been most acutely felt in the dramatic drop in new listings. Residential listings inventory typically grows during late spring reaching a peak in early summer, just in time for the summer homebuying season. The virus has stunted that growth and stopped it entirely in many markets.

There is good news, however. The fall-off in new listing production has begun to reverse itself. In markets throughout the country, rates of new listing production compared to the prior year bottomed out in early April and have been on a multi-week rise since then.

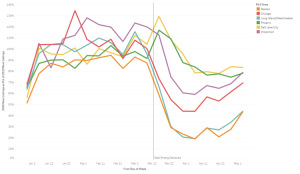

Year over year comparison on new listing production numbers. 2020 vs 2019. Click to enlarge.

Data courtesy of WIREX, MLSPIN, MRED, ARMLS, UtahRealEstate, OneKey MLS’s.

The graph above shows the ratio of new listings signed by week compared to the same week in 2019 for a variety of markets. A few takeaways:

There is much regional similarity. Chicago and Wisconsin follow similar trends, as do Boston and New York and Phoenix/Salt Lake City.

Boston and New York have experienced the deepest drop with new listing production falling to levels 75% -80% below prior year for several weeks in late March and early April (weeks 13-15). This has led to a significant listing shortage in these markets.

Midwestern markets started the year with very strong listing production only to see those numbers dive to levels 40-50% below normal. These markets have been strongly recovering since mid-April.

Western markets have been the least affected with listing production dropping only 25% below last year. These markets have yet to see a recovery in listing production, however and have been stable since late March at 75%-80% of normal levels.

Given the strong return of buyer interest, good weather, and a roll-back of government restrictions we can expect to see the upward trend in listing generation continue.